4 min read

Crude Oil Hedging in An Uncertain Environment - $30 or $200

WTI has traded in a volatile range lately, as have Brent and all other grades of crude oil. The prompt WTI crude oil contract lost more than 8% of...

3 min read

In a recent Bloomberg article, “In a Risky World, Oil Traders Bet on $100 a Barrel” the author explored how, “Some oil traders have started to gear up for a possible price surge as political risks escalate”. If you follow Bloomberg, Reuters, etc. oil reporting, you’ve likely seen one of these articles before as they tend to appear every few months, often using activity in deep out-of-the-money (OTM) options trades as confirmation of a speculative opinion.

Let’s consider what a trader receives when buying call options to see why he or she might purchase $100 calls on December Brent crude oil, which is currently trading around $70/bbl, and if this tells us anything about the trader’s opinion on the future direction of crude oil prices.

When buying a deep OTM call, the trader establishes a position that gains value when either/both the price of the underlying rises and/or volatility rises. The position loses value with the passage of time. The total risk is limited to premium paid. A trader might want this exposure for a variety of reasons. A few examples:

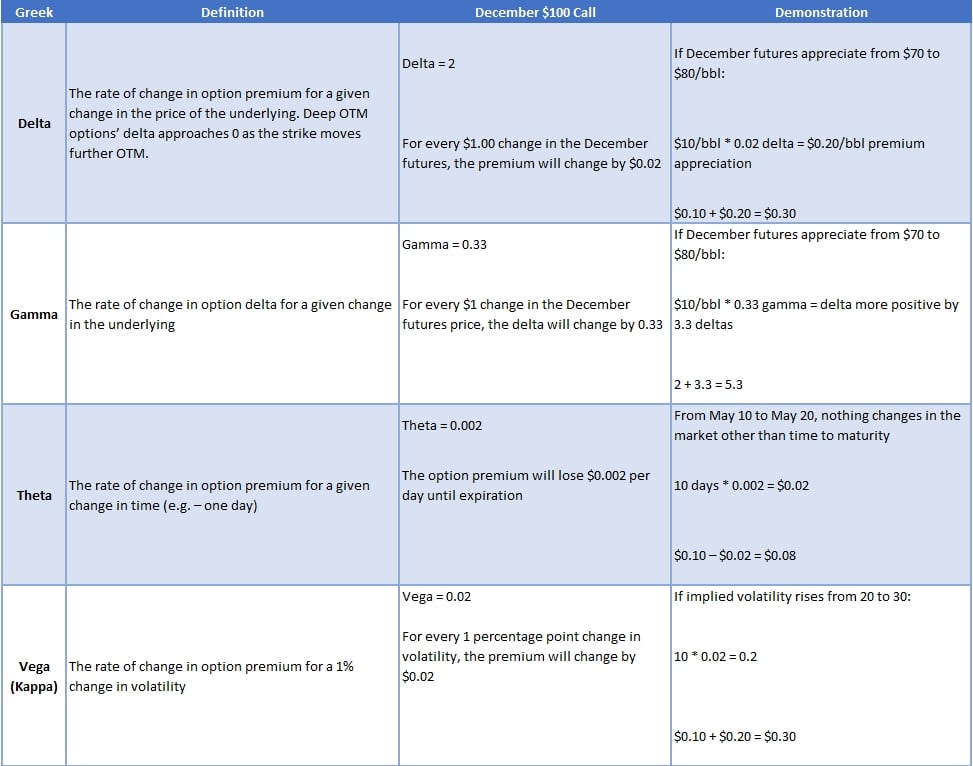

In each of these examples, the call option buyer wants the exposure provided by buying a call option, but none of them are necessarily dependent on the expectation of $100 oil. The trader’s success (profit/loss) is dependent on the options sensitivity to the price of the underlying crude oil future or swap, time, and volatility. An option’s sensitivity to these variables can be calculated using the Greeks, which are summarized in the table below. Assume December Brent is trading at $70/bbl, a $100 call that expires in December has a premium of$0.10, and each change is demonstrated in isolation (“all else being equal”).

As these examples indicate, a trader who is long $100 calls has a lot more to consider than whether the price of Brent will rise to $100 in the next 6 months. An options trader can be correct on market direction, but still lose money because of how volatility and time affect the position. The $100 call is more sensitive to changes in time and volatility than price, so a pure bet on price is an unlikely reason for the spike in volume over the ten-day period the article considers. It seems unlikely (though not impossible) that oil will rebound to $100 between now and December; even less likely that traders are looking at $100/bbl Brent as the foundation of their primary investment thesis.

That being said, there is valuable information to be gleaned from the activity in the options market. At the moment, at least from the perspective of an oil consumer, options appear to be a better, conservative means of establishing a hedge, with a better risk/reward than a pure fixed price hedge such as futures or swaps. Furthermore, call options are currently providing a better value than put options which are similarly or equally OTM, which the author does note at the end of the article. In summary, depending on the risk you need to offset, it’s possible that deep OTM calls could indeed be a valuable component of a crude oil hedging program but as is usually the case, the devil is in the details.

4 min read

WTI has traded in a volatile range lately, as have Brent and all other grades of crude oil. The prompt WTI crude oil contract lost more than 8% of...

2 min read

As we discussed A Beginner's Guide to Crude Oil Options - Part I & Part II, there are four primary factors that determine the price of crude oil, as...

2 min read

As we discussed in A Beginner's Guide to Crude Oil Options - Part I Part II & Part III, there are four primary factors that determine the price of...