2 min read

As Oil Prices Decline, Who is Well Hedged and Who is Not?

Given the decline in oil prices we've recently received several inquiries asking who is well hedged and who is not, particularly among the various...

3 min read

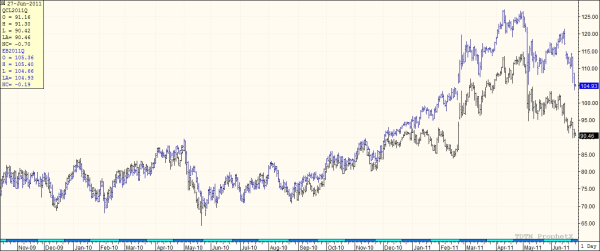

While we generally avoid commenting on news and politics, we thought the announcement from the the IEA last Thursday to release 60 million barrels of crude from reserves, 30 million which will come from the US SPR (Strategic Petroleum Reserve), deserves a few minutes of attention. As the following chart shows, the announcement did push WTI (black) and Brent (blue) prices lower, but prices actually began to decline a couple weeks before the IEA's announcement. That being said, let's look at the reality of the situation.

From the IEA's official announcement:

"The 28 IEA member countries have agreed to release 60 million barrels of oil in the coming month in response to the ongoing disruption of oil supplies from Libya. This supply disruption has been underway for some time and its effect has become more pronounced as it has continued. The normal seasonal increase in refiner demand expected for this summer will exacerbate the shortfall further. Greater tightness in the oil market threatens to undermine the fragile global economic recovery.

In deciding to take this collective action, IEA member countries agreed to make 2 million barrels of oil per day available from their emergency stocks over an initial period of 30 days. Leading up to this decision, the IEA has been in close consultation with major producing countries, as well as with key non-IEA importing countries.

The IEA estimates that the unrest in Libya had removed 132 mb of light, sweet crude oil from the market by the end of May. Although there are huge uncertainties, analysts generally agree that Libyan supplies will largely remain off the market for the rest of 2011. Given this loss and the seasonal increase in demand, the IEA warmly welcomes the announced intentions to increase production by major oil producing countries. As these production increases will inevitably take time and world economies are still recovering, the threat of a serious market tightening, particularly for some grades of oil, poses an immediate requirement for additional oil or products to be made available to the market. The IEA collective action is intended to complement expected increases in output by these producing countries, to help bridge the gap until sufficient additional oil from them reaches global markets.

“Today, for the third time in the history of the International Energy Agency, our member countries have decided to act together to ensure that adequate supplies of oil are available to the global market,” Mr. Tanaka said. “This decisive action demonstrates the IEA’s strong commitment to well-supplied markets and to ensuring a soft landing for world energy markets.”

Total oil stocks in IEA member countries amount to over 4.1 billion barrels, and nearly 1.6 billion barrels of this are public stocks held exclusively for emergency purposes. IEA net oil-importing countries have a legal obligation to hold emergency oil reserves equivalent to at least 90 days of net oil imports. These countries are holding stock levels well above this minimum amount, currently at 146 days of net imports."

This is reeks of political "manipulation" of the oil markets for so many different reasons...

As the previously mentioned data shows, the math simply doesn't add up. If the IEA really felt the need to provide the market with enough oil to compensate for lost Libyan output, they should have said that they were going to flood the market with barrels, (per their own announcement, their members have plenty of inventory), not a trickle of 60MM barrels over the course of a month.

So what does the IEA's announcement or the subsequent release of 60MM BPD mean as it relates to oil prices in the longer term? Only time will tell but 60MM barrels, spread out over the course of a month, simply aren't enough barrels to have a long term impact on the market. In the long run, actual supply and demand (or better said, the market's perception of supply and demand) determines the price of oil, not the IEA, nor any other political or governmental organization. At the end of the day, a physical barrel of oil is only worth what a buyer is willing and able to pay for it.

2 min read

Given the decline in oil prices we've recently received several inquiries asking who is well hedged and who is not, particularly among the various...

1 min read

While the basic fundamentals of energy hedging and risk management don't change very often, the prices at which one can hedge clearly do. As such,...

3 min read

Last December, in a post titled Sovereign State Oil Hedging On The Rise, we highlighted the hedging initiatives of several sovereign oil and gas...