3 min read

Are Airlines Changing Fuel Hedging Strategies in 2014 and Beyond?

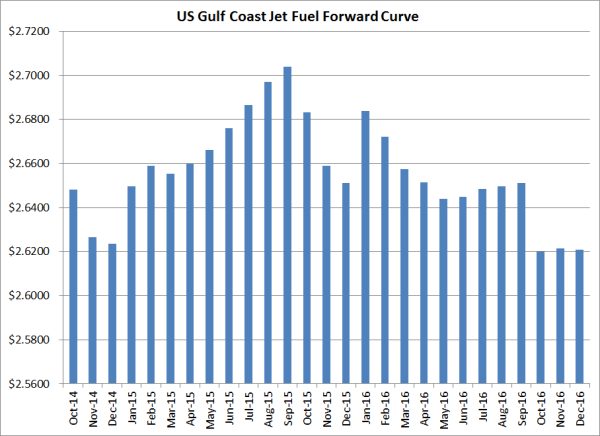

In recent weeks, there have been several articles written on the state of airline hedging in the US, Europe, Middle East and Asia. So, what is the...

2 min read

3 min read

In recent weeks, there have been several articles written on the state of airline hedging in the US, Europe, Middle East and Asia. So, what is the...

3 min read

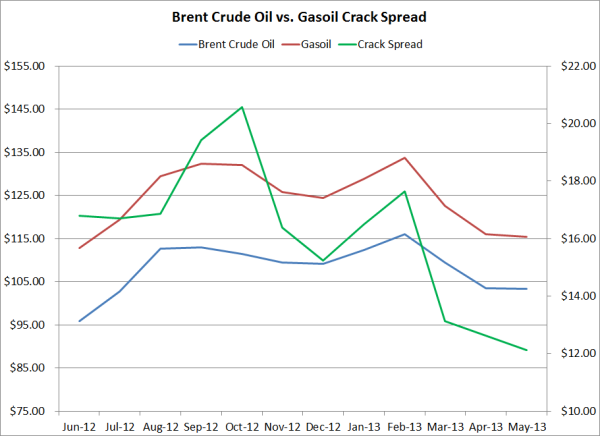

Over the past year, refining profit margins have been quite volatile. As an example, Brent crude oil/gasoil calendar swap crack spreads have traded...

4 min read

I spent the holidays on the road between Houston and Nebraska visiting family. The trip took me though some rural communities where it is common to...