2 min read

Fuel Hedging In Volatile Markets With Call Option Spreads

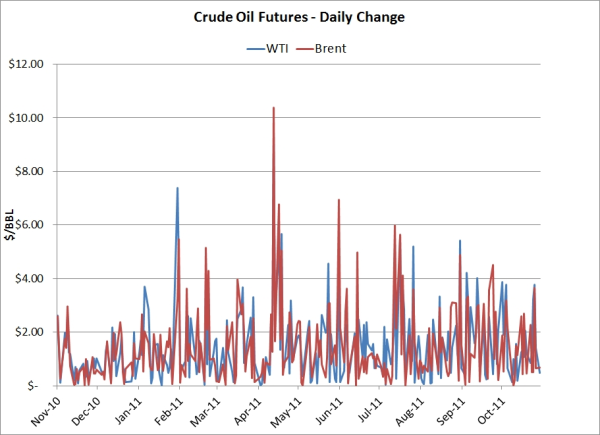

It can't be denied that the recent volatility in the oil and fuel markets is proving to be quite challenging for many companies with active hedging...

2 min read

2 min read

It can't be denied that the recent volatility in the oil and fuel markets is proving to be quite challenging for many companies with active hedging...

3 min read

This post is the second in a series where we are explaining the most common fuel hedging strategies utilized by commercial and industrial fuel...

2 min read

What is a deferred premium option? Essentially, it is identical to a standard call or put option, except that the premium isn't paid until the...