2 min read

Crude Oil Risk Management With Participating Swaps

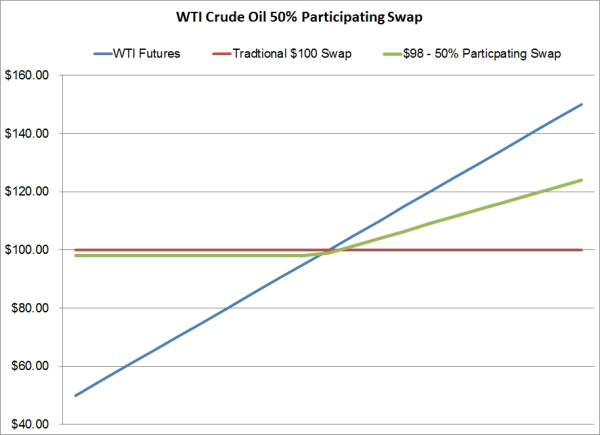

At the request of one of our subscribers, this post addresses how E&P companies can hedge their crude oil price risk with participating swaps. A...

2 min read

2 min read

At the request of one of our subscribers, this post addresses how E&P companies can hedge their crude oil price risk with participating swaps. A...

3 min read

Financial derivatives do not always provide satisfactory risk mitigation. Your risk profile may be more deeply exposed to risks beyond commodity...

3 min read

In recent weeks, there have been a lot of stories floating around about the "oil storage trade" but we've yet to see a good layman's explanation of...