4 min read

A Beginners Guide to Fuel Hedging with Futures

As companies begin to plan for the second half of the year, we’ve been fielding numerous inquiries from companies who are interested in developing a...

2 min read

4 min read

As companies begin to plan for the second half of the year, we’ve been fielding numerous inquiries from companies who are interested in developing a...

3 min read

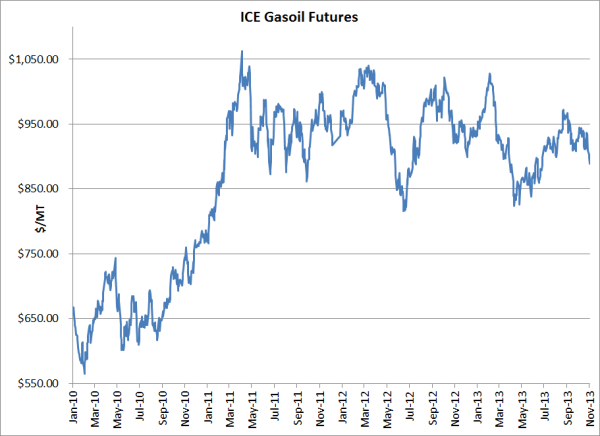

As many companies are beginning to plan for 2014, we have received quite a few inquiries from companies who are looking into hedging their gasoil...

3 min read

This post is the second in a series where we are explaining the most common fuel hedging strategies utilized by commercial and industrial fuel...