3 min read

An Introduction to End-User Natural Gas Hedging - Part I - Futures

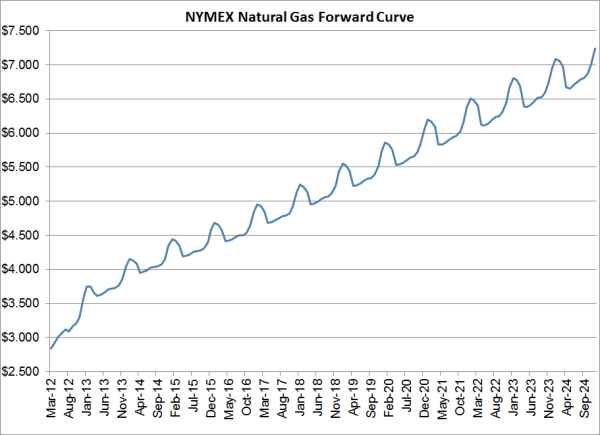

This article is the first in a series of several where we are exploring the various hedging strategies which are available to commercial and...

3 min read

3 min read

This article is the first in a series of several where we are exploring the various hedging strategies which are available to commercial and...

2 min read

This post is the sixth in a series where we are exploring many of the hedging strategies which are available to commercial and industrial natural...

1 min read

As natural gas prices remain depressed, despite the recent bounce, we are receiving numerous inquiries from natural gas producers asking for hedging...