2 min read

Six Tips to Better Manage Your Energy Budget: Hedging & Procurement

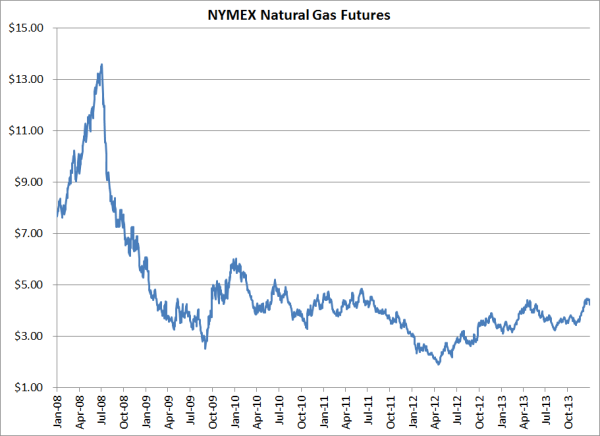

Managing an energy budget can be a difficult task to say the least. Natural gas, fuel and electricity markets are complex and volatile. Not to...

2 min read

2 min read

Managing an energy budget can be a difficult task to say the least. Natural gas, fuel and electricity markets are complex and volatile. Not to...

2 min read

As energy hedging advisors, natural gas consumers, producers and marketers regularly ask us for advice regarding hedging their natural gas price...

3 min read

This post, which explores hedging NGLs with options, is the second post in a series of several where explaining some of the most common NGL hedging...