1 min read

Hedging Strategies As Crude Oil Approaches $50 or $150

Crude oil prices once again traded above $100 today which has many asking, how high will it go, while others wondering if we may see prices collapse,...

1 min read

1 min read

Crude oil prices once again traded above $100 today which has many asking, how high will it go, while others wondering if we may see prices collapse,...

1 min read

As has been well reported elsewhere, Delta Airlines is rumored to be in negotiations to buy ConocoPhillips' Trainer, Pennsylvania refinery in order...

1 min read

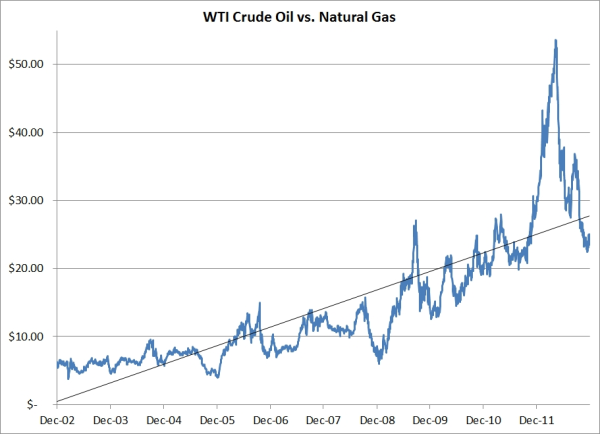

In June of 2011, in a post titled Energy Hedging Myths Demystified - Part I, we took addressed the age old theory that crude oil and natural gas...